529 Account: The Gift Every Parent & Grandparent Should Know About

Every parent knows the feeling. You look at your newborn, your toddler, your kindergartner, and somewhere in the back of your mind, you're already doing the math. College tuition. Room and board. Books. The number is staggering and it's only going up.

And grandparents? The greatest gift you can give your grandchildren isn't just love. It's a head start.

A 529 education savings account is one of the most tax-efficient and underutilized financial planning tools available. At Reliant Wealth Advisory, we set them up directly through our custodian Altruist, making the process seamless, low-cost, and integrated into your broader financial plan.

What Is a 529 Account?

A 529 is a tax-advantaged savings account designed for education expenses. Money grows tax-free, and withdrawals are tax-free when used for qualified expenses including tuition, room and board, books, and even K-12 tuition up to $10,000 per year.

In simple terms, your money grows without being taxed, and you don’t pay taxes when you spend it on school.

For Parents: Start Earlier Than You Think

The most powerful force in a 529 is time. A monthly contribution of $200 starting at birth, assuming a 7% average annual return, grows to over $85,000 by the time your child turns 18. Wait until age 10 and that same contribution gets you less than $30,000.

The tax advantage is real. Every dollar that grows inside a 529 is never taxed on its gains, as long as it's used for qualified expenses. For families in a high tax bracket, that compounding tax-free growth adds up to tens of thousands of dollars over 18 years.

Contributions may be deductible on your state return. Many states offer a deduction for 529 contributions, giving you an immediate return on money you were going to save anyway.

For Grandparents: A Legacy That Lasts

A 529 is one of the most effective ways to transfer wealth to the next generation while reducing your taxable estate.

Federal law allows you to front-load five years of gift tax exclusions into a 529 in a single year. In 2025, a grandparent can contribute up to $90,000 per grandchild ($180,000 for married couples) without triggering gift tax, removing that money from their taxable estate immediately. This is called “superfunding”.

You stay in control. Unlike an outright gift, you remain the account owner. If your grandchild doesn't pursue higher education, you can change the beneficiary to another family member.

Also, A 2024 rule change means grandparent-owned 529 distributions no longer count against a student's financial aid eligibility.

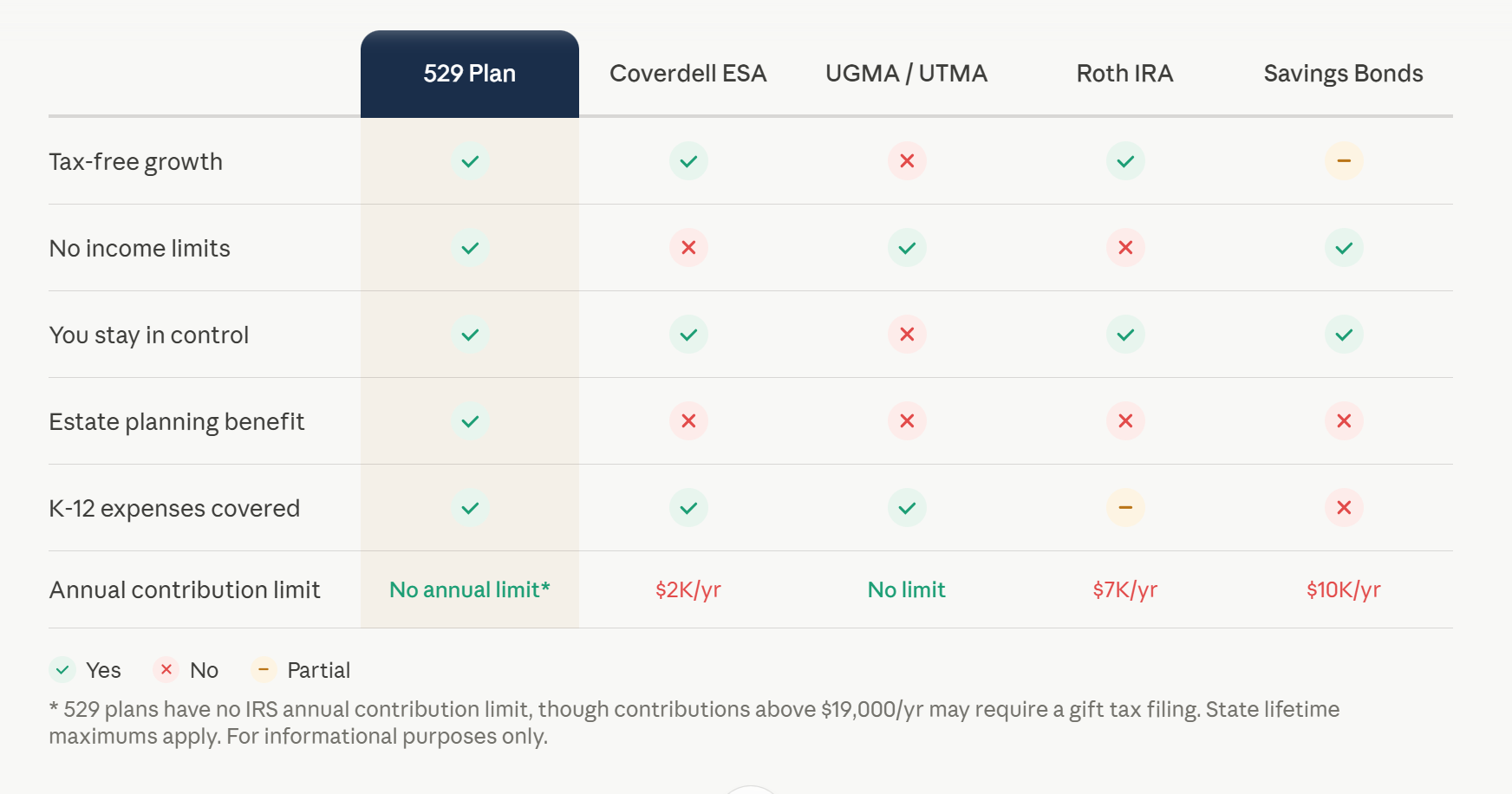

How Does a 529 Compare?

The table below makes it clear: the 529 is the superior way to save for college.

The Limitations

As with anything, there are some limitations on these types of accounts.

The most important is that investment options are limited to the plan's pre-selected menu, typically mutual funds or ETFs. You can’t buy any individual stocks in a 529. Also, excess funds can be rolled to another family member, used for up to $10,000 in student loan repayment, or as of 2024, rolled into a Roth IRA after 15 years.

A few other limitations include: non-education withdrawals are subject to income tax plus a 10% penalty on earnings, allocation changes are limited to two per year, and using an out-of-state plan may forfeit your state tax deduction.

How We Can Help

Opening a 529 is straightforward.

Optimizing it around your tax situation and financial plan is where we add value. At Reliant, we manage 529 accounts through our custodian Altruist, one of the fastest-growing custodial platforms in the country, keeping costs low and everything integrated.

The sooner you start, the longer your money has to compound.

Michael Walstedt is a fee-only financial advisor and founder of Reliant Wealth Advisory, based in Hoboken, NJ. This article is for general informational purposes and may not apply to every individual situation. If this is a question you’re actively considering, a personalized conversation can often bring clarity.