Comparing Today to Previous Bubbles

We've Seen This Before. But Have We?

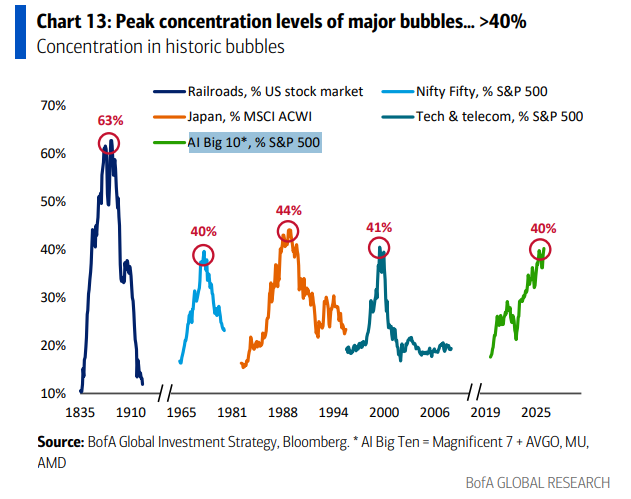

Every major bubble in market history had one thing in common: a small group of companies grew to dominate everything else. And when that concentration peaked, it didn't end quietly.

The railroads peaked at 63% of the U.S. stock market in the 1880s. The Nifty Fifty, the "one decision" stocks of the early 1970s, hit 40% of the S&P 500. Japan's equity market swelled to 44% of the MSCI ACWI by 1988. And anyone who was investing in 1999 remembers tech and telecom reaching 41% of the S&P before the floor gave out.

Today, the AI Big 10, the Magnificent 7 plus AVGO, MU, and AMD, sit at 40% of the S&P 500.

The chart is hard to ignore. The pattern is hard to dismiss.

So Is This a Bubble?

That's the question everyone is dancing around, and the honest answer is: we don't know yet. But history gives us a framework for thinking about it.

What each of those prior concentrations had in common wasn't that the underlying theme was wrong. Railroads genuinely transformed America. Japanese manufacturing genuinely dominated global industry for a generation. The internet genuinely changed everything.

The problem wasn't the idea. The problem was the price people paid for the idea, and the assumption that growth would continue uninterrupted at the same trajectory forever.

What's Different This Time

AI is not a narrative. It's infrastructure. The companies driving this concentration are, for the most part, generating real earnings, real free cash flow, and real competitive moats. That's meaningfully different from the dot-com era, where many of the most hyped names had no revenue at all.

The Magnificent 7 collectively are profitable. They're not being priced on hope alone. That doesn't make them immune to a correction, but it does change the risk profile compared to prior bubbles.

There's also the adoption curve argument. AI may be early innings. If that's true, the market may be right to concentrate capital here, at least for now.

What It Means for Your Portfolio

Whether this ends in a correction or a continued run, 40% concentration in 10 names is a risk worth understanding, especially if you're holding a straight S&P 500 index fund and assuming you're diversified.

You may have more eggs in one basket than you think.

That doesn't mean sell everything. It means know what you own. It means think about whether your allocation still matches your timeline and your risk tolerance. And it means have a conversation with someone who can help you stress-test your portfolio against different outcomes, not just the one where the market keeps going up.

History doesn't repeat itself exactly. But it rhymes often enough to pay attention.

If you’d like to have a conversation, reach out below.

Michael Walstedt is a fee-only financial advisor and founder of Reliant Wealth Advisory, based in Hoboken, NJ. This article is for general informational purposes and may not apply to every individual situation. If this is a question you’re actively considering, a personalized conversation can often bring clarity.